On the Special Relativity of Investment Horizons

When we superimpose our investing principles against modern money-management-industry conventions, we are often struck by the dramatic difference in our investment horizons vs. those of the industry.

At Discerene, we are used to thinking about businesses through more than one economic cycle.

- Because each economic cycle is 7-10 years, this requires us to think about businesses generationally.

- Because of our long holding periods for our investments, we would be happy if we are able to find four new investments a year across our entire team.

- When we make such investments, we fully expect them to experience multiyear “Value Investor’s J-Curves,” i.e., to keep trading down after we buy them.

As a result, one, two, three, even five years seem to us to be quite short timespans. We sometimes forget that these same time horizons may seem like an eternity for shorter-term investors. Hence, we often experience cognitive dissonance when investors ask us why we outperformed or underperformed the market over short (to us) time horizons: If we outperformed, what did we do differently that drove such outperformance? If we underperformed, what mistakes did we make?

We find these questions difficult to answer!

We try to focus such conversations on the businesses we own and our research, letting our fundamental work speak for itself, whatever the recent mark-to-market of our investments. In fact, we’ve usually sowed the seeds of our returns in any given year many years prior. We’ve often studied the companies we’re buying today many years ago and have been patiently waiting for the day when their stock prices got cheap enough for us to become shareholders.

In years past, we’ve wondered why the Nash equilibrium of our industry – not only the investment management industry in particular, but businesses in general – is such a short-term one. In his paper, “Short-Termism at Its Worst,”1 Malcolm Salter identified several important factors behind this phenomenon. We will summarize his work and those of others here.

1. Misaligned Incentives

We believe that it is hard for corporate executives to think long-term if they are overwhelmingly rewarded for short-term results. In their paper, “Duration of Executive Compensation,”2 Radhakrishnan Gopalan, Todd Milbourn, Fenghua Song, and Anjan Thakor developed a metric for “pay duration.” It quantifies the average duration of compensation plans of all the executives covered by an executive intelligence firm’s survey of 2006-2009 proxy statements. The average pay duration for all executives across the 48 industries in their sample was just 1.22 years. We think that such performance-based compensation duration borders on the absurd for leaders of ostensibly multi-decade institutions buffeted by so many factors beyond their short-term control.

Perhaps unsurprisingly, incentives drive behavior.3 Executive-pay duration was longer in firms that spent more on R&D, firms with a higher proportion of independent board directors, and firms with better stock-price performance. Conversely, firms that offered shorter pay duration to their CEOs were more likely to boost short-term earnings with abnormal accruals of operating expenses.

In a survey4 of 401 US CFOs conducted by John Graham, Campbell Harvey, and Shiva Rajgopal, 80% of survey participants reported that they would decrease discretionary spending on R&D, advertising, and maintenance to meet earnings targets. 55.3% said that they would delay starting a new project to meet an earnings target, even if such a delay entailed a sacrifice of value. 96.7% prefer smooth to bumpy earnings paths, keeping total cash flows constant. One CFO said that “businesses are much more volatile than what their earnings numbers would suggest.” 78% of survey participants would sacrifice real economic value to meet an earnings target.

Likewise, Daniel Bergstresser and Thomas Philippon have found5 that the more a CEO’s overall compensation is tied to the value of his/her stock, the more aggressively he/she tends to use discretionary “accruals” to affect his/her firm’s reported performance.

Salter notes: “The risks of short-termism embedded in accounting measures of performance and operating budgets are multiplied when the system for compensating executives fail to provide penalties (such as ‘clawbacks’) when investments or other activities produce losses or are shown to have been achieved by gaming society’s rules. Adding outsized bonuses to no-risk stock options and large rewards, without symmetrical losses when failures ensue, produces a truly toxic situation: personal opportunism combined with short-term risk taking and little regard for long-term effects.”6

This incentive misalignment is exacerbated by the shortening of CEO tenure. In a 2011 study7, Steven Kaplan and Bernadette Minton calculated that the average tenure of large-US-company CEOs since 2000 was <6 years. Kaplan and Minton posited that shorter CEO tenure combined with more stock-based compensation and bigger CEO pay may have created more incentives for CEOs to manipulate earnings8 and magnified short-termism in the firms they lead.9 CEO turnover has not improved materially in the years since. In 2020, the average turnover of CEOs was ~7 years for companies in the S&P500 Index,10 ~6.9 years in the Russell 3000 Index,11 and ~4.9 years in the S&P500 Industrial Index.12

In sharp contrast, a 2019 study13 by James Citrin, Claudius Hildebrand, and Robert Stark of the CEO life cycle found that “some boards part ways with a strong CEO too early after a predictable and often temporary performance slump,” and that some CEOs enjoy their greatest years of value creation after their first decade in office.

Misaligned incentives are exacerbated by the bounded knowledge of corporate directors. A McKinsey & Company study found that a whopping ~50% of 1,016 public directors surveyed across industries and geographic regions had no clear sense of their companies’ current strategy, and only 11% claimed to completely understand the risks their companies faced.14

2. The Ascendance of an Atomized, Disembodied, Speculative, and “Traderly” Financial Culture

Salter also identified competition among investment managers for assets and the desire by managers to minimize business risk as important drivers of modern-day short-termism: “In a world where investors (such as pension funds, sovereign wealth funds, and retail customers) can easily change investment managers, the best way to reduce the risks of such defection is to maintain a track record of consistent, short-term gains, relative to peers. In pursuing such an investment strategy, fund managers naturally communicate to corporate boards and executives a strong interest in quarterly earnings, even when such a short time horizon may compromise long-term value creation. The short time horizon of fund managers is typically reinforced by compensation schemes based on the amount of assets they manage, which tend to rise when their short-term performance is strong. So, too, is fund-manager short-termism reinforced by bonus schemes that pay them multiples of their annual salary when they outperform their peers on some other benchmark on a 12-month basis.”15

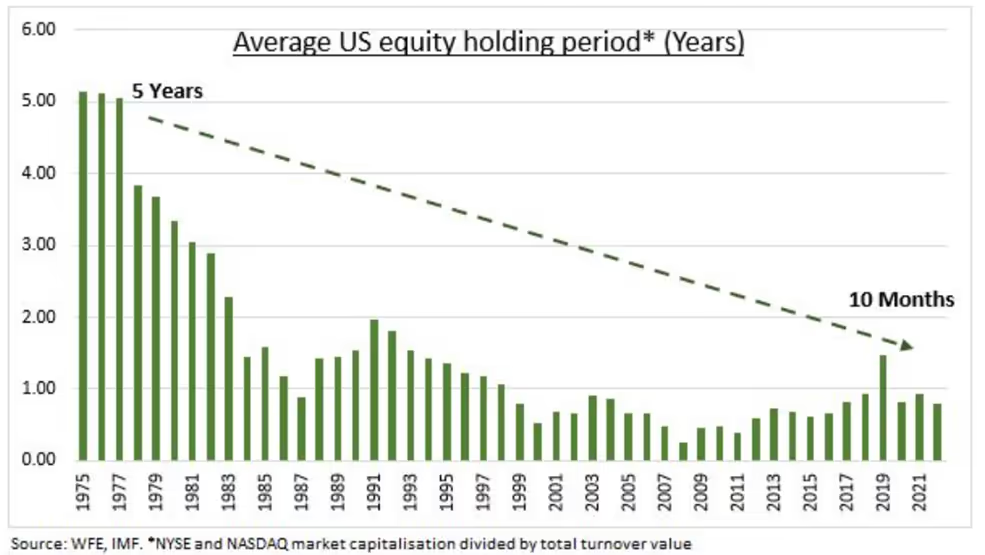

This has been a contributing factor to ever-increasing equities-markets turnover. According to the World Economic Forum and International Monetary Fund, the average holding period of public equities in the US has fallen from >5 years in 1975 to ~10 months in 2022.16

Similar trends are observed in various equity markets around the world.

Senior executives of public corporations have responded to the shrinking investment horizons of their shareholders by offering quarterly “financial guidance” to manage analysts’ short-term stock-price expectations. Ironically, a McKinsey & Company study17 found that providers of such guidance were not rewarded with higher valuations; the only significant effect of the practice was an increase in trading volumes when companies began issuing such guidance.

Indeed, researchers Mei Cheng, K.R. Subramanyam, and Yuan Zhang found18 that companies that offer guidance tend to invest significantly less in R&D than companies that offer guidance only occasionally. Companies offering frequent guidance also had significantly lower long-term growth rates. At Discerene, we view the absence of short-term financial guidance from CEOs and CFOs, along with the lack of pro-forma adjustments to reported earnings, as signals for a company’s culture of long-termism.

Another effect of short-termism has been to encourage firms to shed or outsource functions formerly considered to be critical to businesses, including R&D, manufacturing, sales, and distribution, thus creating atomized and fragile slivers of businesses that nevertheless often command illogically lofty valuations. For example, in recent times, aerospace, pharmaceuticals, and software companies that do not attempt to sustain going-concern investments and instead seek to continually acquire other companies in order to hollow out such companies’ engineering, R&D, and/or sales/distribution teams — thereby eliminating all possible sources of competitive advantage — have been feted as “asset-light” and “high-ROIC” poster children of their respective industries.

Just like that, the corporations that become the darlings of modern capital markets get curiouser and curiouser.

3. Gresham’s Law

Named in 1860 by economist Henry Dunning Macleod after Sir Thomas Gresham, a sixteenth-century English financier, Gresham’s Law is a monetary principle stating that “bad money drives out good.”19

In a 2010 speech20, Andrew Haldane, then Executive Director of Financial Stability at the Bank of England, expressed concern about the effects of Gresham’s Law on short-termism in financial markets. To illustrate his point, he described three archetypical classes of investors:

- Impatient short-term speculators who follow the momentum of the herd, buying when prices are rising and selling when they fall;

- Patient, long-term investors who invest according to where prices are relative to their long-term fundamentals;

- Untested investors who can mimic either the speculator or the long-term investor, but whose returns are assessed at frequent intervals and who withdraw or add funds accordingly.

Short-term speculators cause deviations from intrinsic value while long-term investors drive prices back toward intrinsic value.

As in many social systems, there are two very different equilibria.

- In Equilibrium X, patience wins the day. The performance of untested investors pursuing momentum strategies falters while that of those pursuing long-term fundamental strategies flourishes. The proportion of patient, long-term investors rises.

- In Equilibrium Y, large numbers of short-term speculators cause prices to deviate sharply from fundamentals. Among untested investors, momentum strategies flourish while long-term fundamental strategies fail. The proportion of speculators rises, increasing the degree of misalignment of prices, and in turn driving out the long-term fundamentalists. Lummox money drives out good.

Salter pointed out that modern-day financial-markets trends have tilted financial markets towards Equilibrium Y. For example, in financial markets, information is generally perceived as a good thing. However, the over-availability of information has reduced the half-life of marginal news flow to that of a tub of ice cream on a hot summer day. In response, companies have migrated from holding annual general meetings to adopting quarterly reporting cycles to providing steady streams of almost real-time trading updates. Today, traders relying on an “information edge” are willing to pay a schoolteacher’s lifetime wages to alternative data sources for small handfuls of KPIs tracked right down to a daily frequency, and single tweets can change the valuations of companies by tens of billions of dollars.

Liquidity is likewise double-edged. The availability of liquidity can reduce the impact of trading on market prices. However, it also provides short-term speculators with sufficient firepower to drag market prices sharply away from fundamentals for long enough to drive large swaths of intrinsic-value-based investors out of the market.

The application of Gresham’s Law in financial markets has also been exacerbated by whiplash monetary policy.21 In particular, free money tends to attract speculators and crowd out rational, intrinsic-value-based investors, thereby — perhaps counterintuitively given the (mistaken) conventional wisdom that low discount rates enable long-duration investments — shrinking investment horizons:

- In the short term, changes in the marginal demand/supply of printed money dominate the actual operating cash flows of businesses in driving valuations.

- Over time, this drives out investors playing the “weighing game” (i.e., those focusing on trying to estimate the intrinsic value of businesses) and attracts speculators playing the “expectations game” (i.e., those focusing on trying to predict marginal changes in expectations or sentiments about the future).

- As money printing accelerates, the expectations game gradually reduces to hanging on to every one of a single human being’s “Freudian tells.”

At Discerene, we sometimes feel like we’re sitting outside the financial-markets “Matrix,” where we watch the short-term, speculative behavior of so many market participants from a mirthful distance.

Modern capitalism can be laugh-out-loud funny!

4. Asset-Liability Mismatches

Finally, we believe that it is difficult for management teams and investors to think and behave long term if the source of their capital itself is short term.

The cost of asset-liability mismatches in financial institutions came back in the headlines in 2023 because of the failures witnessed at Silicon Valley Bank, Signature Bank, Credit Suisse, etc. We believe that asset-liability mismatches are even more prevalent, and more dangerous, in the non-bank financial and corporate sectors. For example, many entities, including money-market funds, mutual funds, hedge funds, venture/private-equity funds, and corporations have far shorter-term equity and debt capital than the average duration of their assets.

This mismatch is not problematic so long as asset prices keep rising and capital inflows exceed outflows. Borrowing short and/or raising highly liquid equity capital and lending/investing long has a seductive appeal during loose monetary policy regimes and in rising markets. However, we believe that many investors will continue to be shocked by how quickly and badly things can unravel.

The Swinging of the Pendulum

How do we respond to these trends? We don’t.

Fortunately, because financial markets are reflexive22 and self-correcting, Gresham’s Law leads to partial, not general, equilibria. For example, if there are too many active investors in the market, it becomes difficult for many active investors to generate excess returns, driving out many such players. Conversely, if there is too large a proportion of passively managed assets in a financial market, the few active investors in such market will generate healthy supernormal returns.

Similarly, the very ascendance of short-term financial-markets speculators in recent years has sowed the seeds of their downfall. As asset prices were dragged further and further away from their intrinsic values, each marginal wave of speculators drove the previous breed out with ever more extreme momentum-driven strategies. Thus, the “high-quality compounder” momentum investor who was prepared to shell out >40x earnings for Nestle Nigeria in 2014 was replaced by an even more dimly valuation-aware speculator who was willing to pay >10x revenues for Takeaway in 2018, who in turn was replaced by a willfully analytics-free speculator who, in an ecstasy of fumbling, was prepared to pay any price for Rivian in 2021. When the money printing ends and the speculative fever breaks, such speculators are then flushed out of the industry.

One looks left, right, up, down, and all around, and sees not an abundance of bona fide value investors left standing.

The hollowing out of the value-investor community creates massive mispricings of real companies with genuine reasons to exist, sustainable business models, actual cash flows, and defensible barriers to entry (or “moats”).

This leaves the few that remain with an investing environment that looks like a breath of spring.

1. Salter (2013), “Short-Termism At Its Worst: How Short-Termism Invites Corruption… and What to Do About It,” Edmond J. Safra Working Papers, No. 5, Harvard University.

2. Gopalan, Milbourn, Song, and Thakor (2013), “Duration of Executive Compensation,” Journal of Finance, forthcoming.

3. To quote Charlie Munger: “Well, I think I’ve been in the top 5% of my age cohort all my life in understanding the power of incentives, and all my life I’ve underestimated it. And never a year passes but I get some surprise that pushes my limit a little farther.”

4. Graham, Harvey, and Rajgopal (2006), “Value Destruction and Financing Reporting Decisions,” Financial Analysts Journal, 62(6).

5. Bergstresser and Philippon (2006), “CEO Incentives and Earnings Management,” Journal of Financial Economics 80(3).

6. See supra, footnote 1.

7. Kaplan and Minton (2011), “How Has CEO Turnover Changed,” International Review of Finance 12(1).

8. Kaplan and Minton (2006), “How Has CEO Turnover Changed? Increasingly Performance Sensitive Boards and Increasingly Uneasy CEOs,” Working Paper No.12465, National Bureau of Economic Research, Cambridge, MA.

9. See also Rumelt (1987), “Theory, Strategy, and Entrepreneurship,” in Teece, ed., The Competitive Challenge, Harper & Row, New York; Jensen and Meckling (1979) “Rights and Production Functions: An Application to Labor-Managed Firms and Codetermination,” Journal of Business 52; Jacobs (1991), Short-Term America: The Causes and Cures of Our Business Myopia, Harvard Business School Press, Boston.

10. Petro (2022), “Executive Churn in Retail C-Suites Is Unsustainable,” Forbes.

11. Tonello and Schloetzer (2021), “ CEO Succession Practices in the Russell 3000 and S&P 500,” Harvard Law School Forum on Corporate Governance.

12. See supra footnote 9.

13. Citrin, Hildebrand, and Stark (2019), “The CEO Life Cycle,” Harvard Business Review.

14. Shelton and Fritz (2005), “The View from the Boardroom,” McKinsey Quarterly, March 2005.

15. See supra footnote 1.

16. Laider (2023), “The Costs of Rising Short-Termism,” Global Market Insights.

17. “Weighing the Pros and Cons of Earnings Guidance: A McKinsey Survey,” McKinsey Quarterly, March 2006.

18. Cheng, Subramanyam, and Zhang (2005), “Earnings Guidance and Managerial Myopia,” Columbia Business School.

19. For more background, see, e.g., Wikipedia's entry on Gresham's Law.

20. Haldane (2010), “Patience and Finance,” speech at the Oxford China Business Forum, Beijing, September 9, 2010.

21. See also: Chatterjee and Adinarayan (2020), “Buy, Sell, Repeat! No Room for "Hold" in Whipsawing Markets,” Reuters.

22. See also George Soros’ writings on this topic.